Can Leasing be Made More Affordable?

Ministry of Civil Aviation Secretary R. Choubey recently called for greater participation from policy makers and users to promote MRO services, offer training, and provide more attractive leasing packages that could spur new initiatives for improved regional connectivity

As any start-up airline can attest, a war chest of cash is an essential thing to have on the company’s checklist prior to the first flight. Notwithstanding the expenses associated with launching service and day-to-day operations, a huge cash outlay for initial deposits and pre-delivery payments for the purchase of a fleet of new aircraft isn’t always an option. Without a previous track record or sterling credit history, a carrier’s inability to qualify for traditional financing or its reluctance to assume the risk of asset ownership means that leasing is often the most economical and sensible alternative, even in today’s low interest rate environment.

Revenue in Rupees. Expenses in Dollars

The Ministry of Civil Aviation Secretary Rajiv Choubey’s call for lower aircraft lease rates is likely a consequence of the country’s chronically low domestic airfares that generate the lowest revenue per passenger-kilometre compared to local yields in Japan, Indonesia, Australia and Malaysia, according to first-quarter 2016 IATA data. Reducing the cost of leasing aircraft would certainly benefit fledgling regional airlines yet rentals are commonly paid in US dollars or euros. The strength of those currencies against the rupee poses a real challenge for carriers to earn sufficient revenue to cover not only the monthly lease expense, but other dollar-based costs as well, like fuel. Given the number of new aircraft and seats to be added by AirAsia, IndiGo, SpiceJet and Vistara, it’s unlikely that domestic airfares will rise any time soon. If fares won’t go up, operating costs must come down.

Supply, Demand, Timing and Technology

Anticipating the need to replace the world’s ageing narrow-body fleet, aircraft lessors went on a shopping spree between 2007 and 2010. Their acquisitions were welcomed by airlines who found themselves restricted by tight access to capital following the 2008 contraction in financial markets. With oil above $100 a barrel and airline balance sheets awash in red ink, narrow-body lease rates were under pressure by 2011-12, a reflection of too much supply and not enough demand.

The high price of oil prompted manufacturers to introduce more fuel-friendly, technologically-advanced, high-efficiency aircraft. Even with the A320neo, B737 MAX, E-Jets E2 and CSeries on the market, narrow-body lease rates were recovering from their 2013 lows by last year. Today, for regional airlines wanting to access Tier-II and Tier-III cities with smaller jet equipment, the strong US dollar, inventory of aircraft available for lease, and market rates still aren’t conducive to attracting new regional entrants as the Ministry of Civil Aviation is hoping.

Age and Size Important

The balance of aircraft supply and demand often determines market rates with older, less economical jets offering the cheapest rents. They may be a bargain to lease, but the trade off is usually high operating costs, high fuel consumption, and the need for heavy maintenance during the term of the lease. Moreover, there can be significant costs to reconfigure leased aircraft to ensure they are compatible with the local market profile. Premium cabins, for example, have rarely been successful on regional routes.

Are regional airlines in India doomed to be dumping grounds for old airplanes? Flying those fuel-hungry, high-maintenance low-rent jets to domestic Tier-II and Tier-III cities may seem like an inexpensive way to provide seats, but scheduling all their excess capacity in low-demand markets encourages fare dilution and weak, unsustainable yields. Even though smaller, newer aircraft may command premium rents, their lower operating and obsolescence costs and ability to generate higher unit revenue (up to 30 per cent higher, according to Embraer) often make them more economically viable.

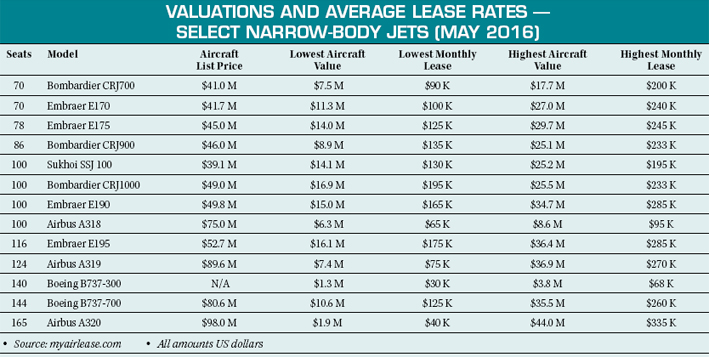

May 2016 valuations and sample average lease rates for regional and narrow-body jets published on MyAirlease.com (referencing recent transaction history and manufacturersourced prices) show how smaller aircraft with their lower operating costs command premium monthly rents.

Can Rates Go Lower?

Lease prices are a function of supply, demand and aircraft age. Since a lessor’s portfolio of airplanes can be placed anywhere around the world, they often seek the most creditworthy, reliable prospects that are operating in a stable environment. Leased aircraft are unique assets. Their mobility allows the lessor to go where there is opportunity and to price monthly rents accordingly. Carriers with weaker financial footings and poor track records will find their lease rates incorporate an element of risk should they fail. Lessors then incur repossession and remarketing expenses.

In this cycle of continued growth in passenger enplanements and fuel price volatility, new, leased aircraft are in demand. Consumers have become more sophisticated and expect newer-technology airplanes, which they often equate with safety. The expanding fleets of India’s main domestic carriers reflect the trend to new equipment. Any acquisitions of very old, low-rent, over-capacity jets by regional airlines would be incompatible with the drive for greater efficiency in such a competitive domestic landscape.

Regional carriers in India may not have much bargaining power in this upward-moving market where lease rates for new aircraft are not heavily discounted. Short-term gain renting big, old, cheap airplanes may incur long-term pain when the price of fuel inevitably rises or the rupee slides against the US dollar.

The author is an airline industry veteran for 35 years. He was a former domestic airline pricing director for Air Canada and global marketing director with some aircraft manufacturers.

SP's AirBuz - CURRENT ISSUE